My meeting with "the banker"

My meeting with "the banker"

I was invited to meet with an exec of a big bank. I recap it.

It’s October 27, 2023, and I recently met with a banking exec. Here are some broad takeaways.

A couple of weeks ago, I was invited downtown to meet with a fairly high-ranking executive at one of the biggest banks in the world. It was sort of a press meet-and-greet type of thing. Nothing too formal. But it was planned months in advance, and I agreed to go – you never know how many opportunities you’re going to get, after all.

What intrigued me about the invite was that I…don’t think of myself as a “friend” of the banks. Certainly not the big ones. I remember seething all those years ago during the financial crisis, and a lot of my ire was targeted at the big banks and Wall Street – justifiably so, I think. I even had my own personal “Occupy Wall Street” moment in suburban Seattle, as I strutted into my local Chase branch (my accounts were at Washington Mutual, which collapsed and was taken over by Chase) and told them I wanted to close my accounts.

I opened new accounts at the largest local credit union in the Pacific Northwest, where they remain to this day, and Chase lost out on literally hundreds of dollars in customer accounts that day. I did speak with the branch manager, interestingly, who asked why I was moving to another institution. I said that I didn’t appreciate the bank’s behavior in the run-up to the then-current economic cataclysm. He nodded and wished me good luck.

Now, I was fresh out of school. I had three jobs. There was a time when I had four jobs. It was ridiculous. I was salty. I still am. And as we all know, the big banks largely walked away from it unscathed. Some collapsed, but others came out stronger.

Anyway – this is all to say that, in my head, I was wondering if the people inviting me to their gorgeous glass tower in Manhattan knew who I was, and what I thought of them. Apparently not. So, I agreed to go.

Given it was an off-the-record conversation, I won’t say who I talked to or where, but I do think it’s worth discussing, in broad terms, some of the things we talked about, and what I took away from the conversation. Again, if this were 15 years ago, I probably would’ve gone all punk rock on them, but, you know, if you want answers and solutions, you need to have a little tact.

So, I made the trek from where I live north of New York City into Manhattan, and was met in the lobby by a very nice young woman who took me to one of the building’s upper floors. It was quiet. A lot of security. And very upscale. I imagine it would be like working in a Four Seasons or something. And the views outside? You could stare in any direction, out any window, for hours. I’m a West Coast boy at heart, but New York City, in its mammoth glory, really is a sight to behold if you can get above street level.

I was then led and introduced to – let’s call this person “the banker.” The banker was perfectly pleasant. Very nice. I like them. And we sat down and chatted for 30 minutes about all sorts of stuff, but I did manage to gain some perspective from the upper echelons of the financial universe. This is good. It’s helpful. It helps me do my job, and it helps me shape my thoughts and feelings about things in a more rounded way.

I will say that I don’t think these people are out to destroy us plebs, though it may feel like it sometimes. They’re simply caught up in what I think is a rather destructive cycle of short-term thinking: They need to get the numbers up for their quarterly reports, and that’s their job. So, they do what they need to do to do their job. It’s not always good, and it’s not always bad.

But from the average American’s perspective, it can look nefarious, oftentimes. I guess if you are working in a high-level, high-impact position – imagine you were the president, for instance – it can really be hard to grasp how big of a ripple effect seemingly small decisions can have on people that you’ll never meet or see. I struggle with this in my writing – I may express an opinion or write a sentence that, in my mind, is fairly innocuous. I’m just a guy, in my house, typing on a keyboard. But I forget that people around the world – millions, over the years – have read the words I’ve written in my small office. Not everyone is going to absorb the words in the way I intend. It’s…often hard to keep in mind.

But back to the meeting.

There were a few things that I gleaned from my meeting that I feel are worth highlighting. Again, nothing specific, but I think it can be helpful to get some insight into how some people in finance – a world that often feels like it’s in another orbit, or in another universe – are thinking about the issues and concerns of us normal working people.

On the economy: nothing unexpected, really

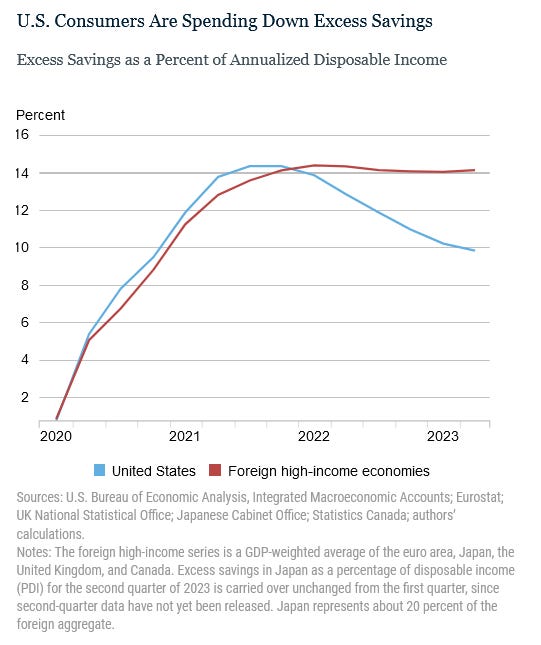

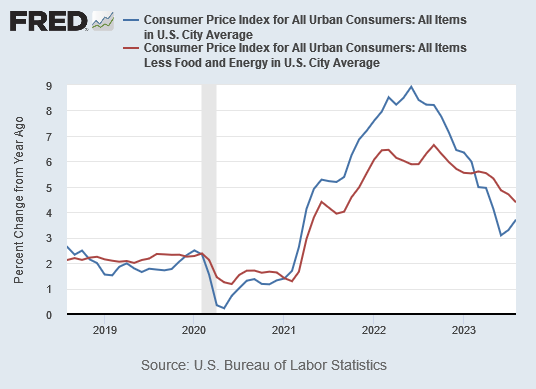

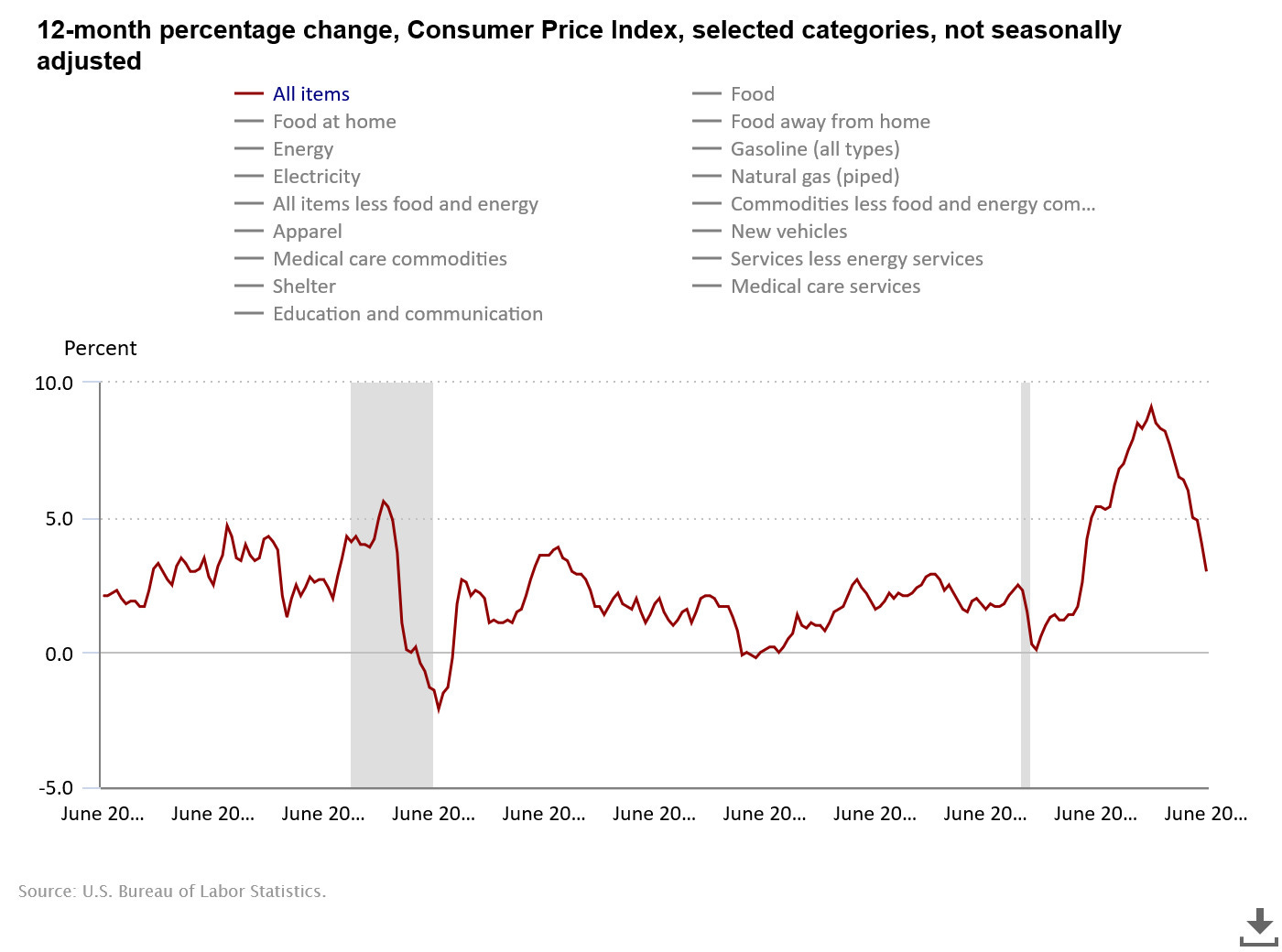

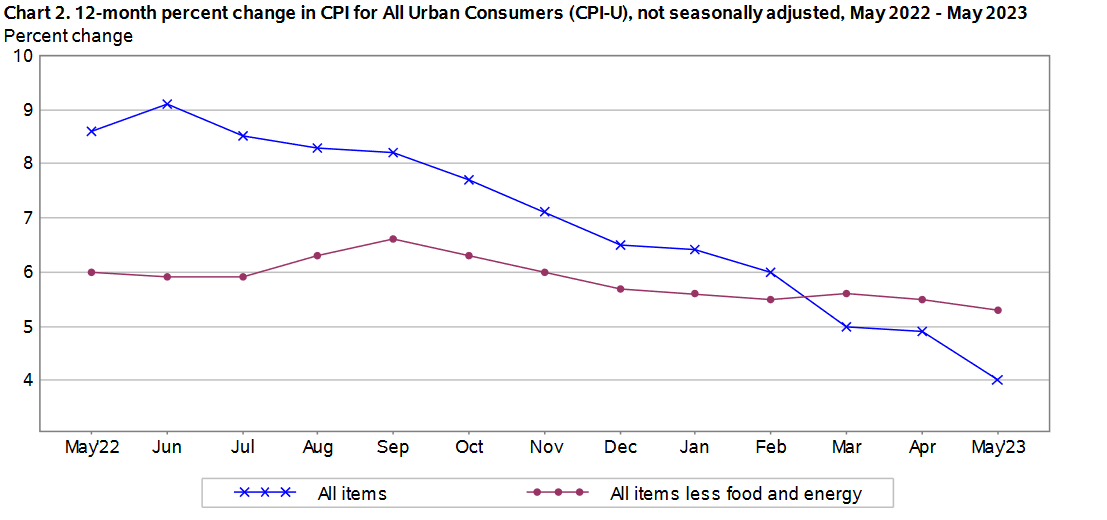

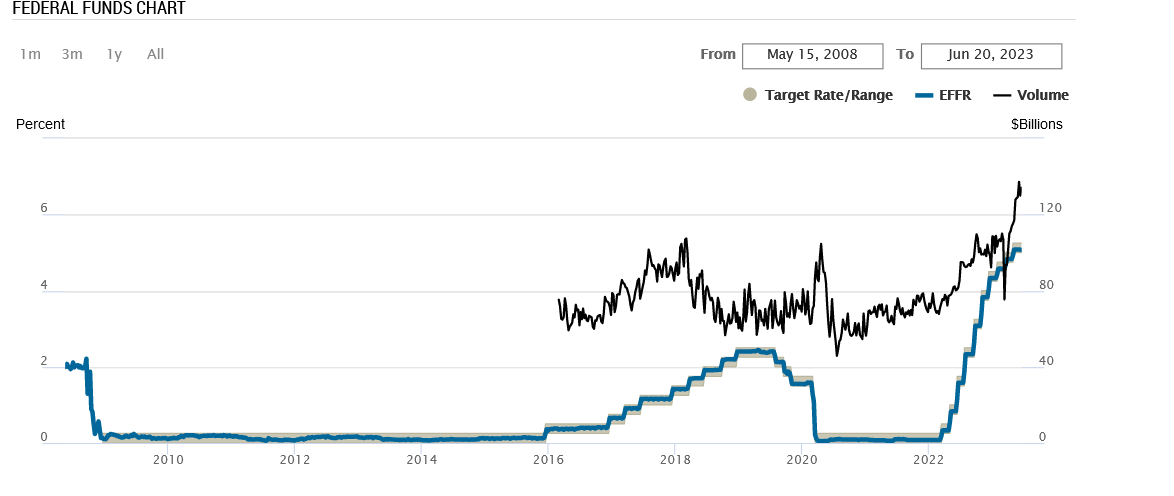

I’ve written about how many people are struggling to figure out whether the economy is good or bad right now – as I always say, it doesn’t really matter, it just “is.” But given recent blockbuster jobs reports and more recently, a GDP report that blew the doors off the building, it’s really hard to say that we’re in a recession.

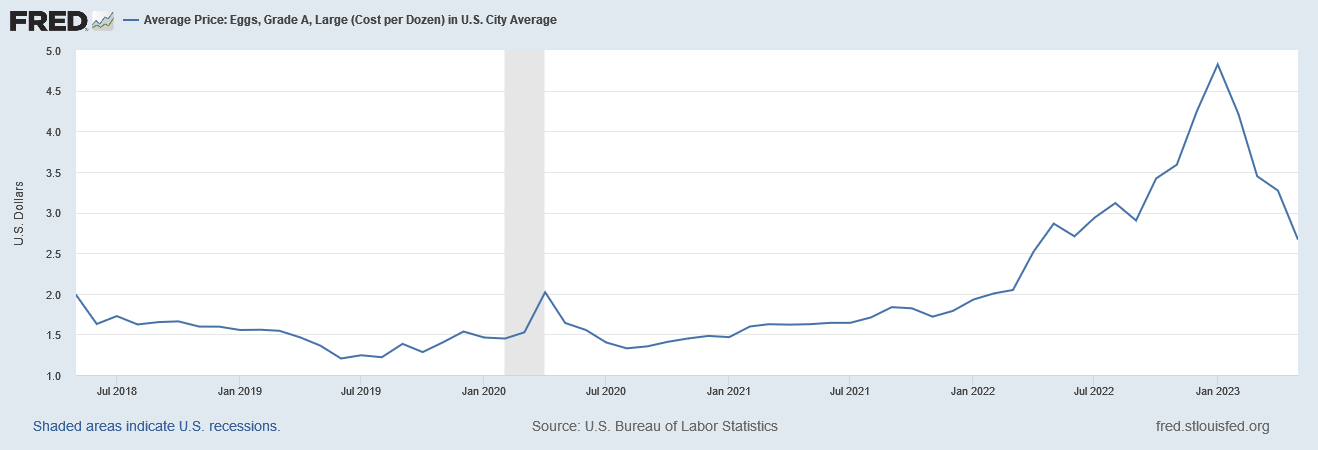

Alas, many people think that we are. Price increases and layoffs in many industries have people in a pinch, and they don’t feel good about things.

So, I asked the banker: What’s the deal? Their response? What we’re seeing is more or less what was expected. We’re not all the way out of the woods in relation to the shock waves of the pandemic. Things are still settling down and sorting themselves out – including supply chains and inflation – and it’ll likely be a couple more years before they really are. So, there’s no panic coming from the top. That’s not to say that there aren’t problems, they told me. But there aren’t really huge concerns that we’re about to fall off an economic cliff.

They’re aware that people are hurting

On a similar note, I asked how banks are looking at prevailing sentiment surrounding both banks themselves, and the economic environment. The banker said that they’re not unaware of how many people perceive them, first and foremost. That’s a big reason that many large banks are bringing in some big changes. Again, in broad terms, many banks are getting rid of fees, they’re making their products simpler, and some are even remodeling their branches to make them a bit more welcoming.

This is all in an effort to shift and win over more customers. That’s a start, right?

They’re also keeping an eye on customers’ financial health. While they may not be watching your bank account, they do see trends and can come away with some data points about what’s going on with consumers’ finances. Right now? Yeah, people have less savings and many are feeling the squeeze. But what seems clear is that not everyone is struggling, and by and large, consumers seem to be on more sound financial footing than even individuals themselves may believe.

Take that how you will.

Relationships: The next big thing

Finally, the banker and I discussed relationships – not our personal relationships, of course, which is always fascinating – but relationships with financial institutions. That’s going to be a big focus of banks in the years ahead. It’s already a big focus for many companies. Think about all the work that goes into Apple or Google or Amazon fomenting a “relationship” with customers – getting them into an ecosystem, and fostering the relationship for years to come.

Banks do this already, but I get the sense that this will become a big focus in the years ahead. Again, I do think that people hate banks. There’s good reason for that, too. And I think that at least some of them are trying to mend that relationship and create lifelong customers.

I’ve said it before: I think people should switch banks more often. But they generally don’t. That’s likely the primary reason banks have been so unresponsive to customer concerns in years past. That does seem to be changing.

I could go on. But those are some of the key takeaways from my meeting with the banker.

Numbers and links

Go see a star war: The Space Force unveiled its first official painting showing a space battle. (Space.com)

24 hours: A look at the “average human day.” (Scientific American)

Tax talk: When we discuss the budget deficit, why don’t we talk about revenue? (Marketplace)

C’mon man: My congressional representative pulled a fire alarm to stall a vote. I expect better. (The New York Times)